Insurance companies have traditionally lagged in modernizing their core applications. Most CIOs want to have a modern system, but they often cite a number challenges to core transformation:

Logic behind sticking with the legacy system

1. If It's Not Broken, Why Fix It?

Most insurance companies would state this logic: Why should we replace the old system; what’s the problem?

The fundamental concept companies must understand is the way they measure problems. If you measure problems only with broken status, then maybe a system can still work until it is fully broken. But market dynamics depend on many other factors, like competition, speed to market, operational cost, goodwill, etc., and each company should evaluate the definition of "broken" and then evaluate the legacy system.

If you are not improving your core parameters like sales, market share and reduced operations costs on a quarter-on-quarter basis, your systems may be broken.

2. It’s Too Costly

Of course, there is a cost involved. Core admin systems are assets of your organization, so the investment is inevitable. The questions to ask are: What’s the benefit? How long will it take to get up and running? Can the overall transformation process be predicted?

It is important for the insurance company to get some help with transformations rather than try to do everything by themselves. It is critical to see if the vendor has done such transformations. Do they have any strategy to stick around to support the system? How are they investing themselves in building value-added solutions?

See also: Core Systems: Starting a Whole New Game?

3. It’s Risky to Replace

The insurance industry knows that there is risk everywhere, but the question is how we manage and mitigate it. Risks associated with such replacements are:

- Cultural Risk – As part of transformation, companies should plan for a cultural shift, not only within the organization but also with all the stakeholders, such as agents, partners and finally the customers.

- Fit Risk – Will the new system fit into the unique way of working in your organization? An essential point to remember here is that the more you try to be unique, the more it will be difficult to upgrade. Too much differentiation will make your new system a legacy in a few years, as it will not be able to upgrade easily.

- Scope/Time/Cost Risk – These are linked and should be monitored closely. Working with experts who are known for managing large transformation programs could mitigate this risk. Different management and contract styles have shown different results. For example, a large and complex program is best managed as an agile project.

Companies get slightly confused about the legacy platform. Should they think about whether to replace systems based on resources or on whether there is a problem with the system's fundamental architecture? The architecture of the application should support faster speed to market and better and faster customer service, and it should be central to the organization's digital strategy. Don’t focus on skill availability; concentrate on the application's capability.

Choosing the approach

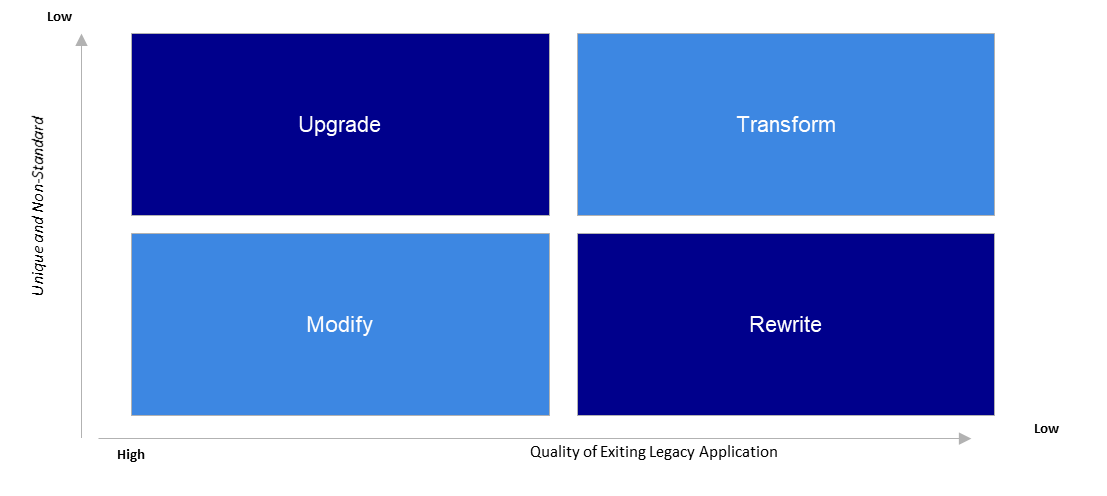

Core modernization is no longer optional, but choosing an approach can be classified into four buckets depending on: a) how unusual your requirements are and b) the quality of the existing system. While deciding the approach, one should always keep in mind the big picture of organizational growth strategy and changes in customer expectations in the digital world.

Decision Chart: Core Admin Evaluation chart.

High Quality - Unique Process (Modify): Companies that have acquired or developed an application recently with modern architecture should stick with the existing platform. However, they should continuously try to add functional as well as technical features to the system to keep it current.

Low Quality - Unique Process (Rewrite): One of the predominant reasons for rewriting or custom-building applications is the lack of commercial off-the-shelf (COTS) products available to support the unique needs of the insurer. We still suggest looking for a specialty risk product in the market, but rewriting a sleek application is also an option. The key benefit of rewriting is that we can reuse some key assets, like business rules and data sets. Before deciding to rewrite into a better architecture, there are two points to consider–

- Is it worth sticking to existing processes or will it be better to move toward standardization with some deviation, i.e. some customization to existing COTS products?

- Do we intend to solve a single core admin system problem or to support the entire IT ecosystem?

High Quality - Standard Process (Upgrade): Companies already having a COTS product should plan for regular upgrades of the application. While insurers purchase standard products and configure them to their needs, they normally don’t plan for an upgrade as additional time and budget. This leads to the challenge of an unsupported version. Companies should not only plan for application upgrades but also infrastructure upgrades. Most insurance COTS products come with major and minor upgrades. Minor upgrades will provide bug fixes and security enhancements, but all major upgrades will require adoption of new features and functionality, training of staff and technological adoption based on industry standards. Enterprise applications, unlike mobile apps, require a bit of handholding before we can upgrade. So here is a serious suggestion: Budget for upgrades. If you don’t, one day you will require a transformation budget.

Low Quality - Standard Process (Transform): Many insurance companies are stuck with the old core admin system, which is difficult to change, and have adopted "modify" as a strategy. Lack of documentation, skilled resources and technological compatibility make these applications painful to maintain. They pose some serious operational challenges and restrict the growth of the organization. The insurance industry is full of niche software providers and many COTS products that provide some great applications and lots of in-built standard processes. One should perform a full-blown search to find such players for a long-term solution. Companies should do a better fit gap analysis for their long-term needs before selecting a core application. They have the choice to select best-of-the breed applications or the full suite for their core needs.

See also: Finding Success in Core Systems

Conclusion

Customer expectations are changing rapidly. To keep up with the competition, insurance companies should regularly evaluate the capabilities of their core admin system to support business growth. They should use the matrix mentioned above to categorize each application into the four buckets. CIOs should do this evaluation every three to six months to ensure that IT is always ready to support the growth and service demands of the business.