The property/casualty industry has been characterized by its market cycles since… well, forever. These cycles are multi-year affairs, where loss ratios rise and fall in step with rising and falling prices. In a hard market, as prices are rising, carriers are opportunistic and try to "make hay while the sun shines" – increasing prices wherever the market will let them. In a soft market, as prices are declining, carriers often face the opposite choice – how low will they let prices go before throwing in the towel and letting a lower-priced competitor take a good account?

Many assume that the market cycles are a result of prices moving in reaction to changes in loss ratio. For example, losses start trending up, so the market reacts with higher prices. But the market overreacts, increasing price too much, which results in very low loss ratios, increased competition and price decreases into a softening market. Lather, rinse, repeat.

But is that what’s really happening?

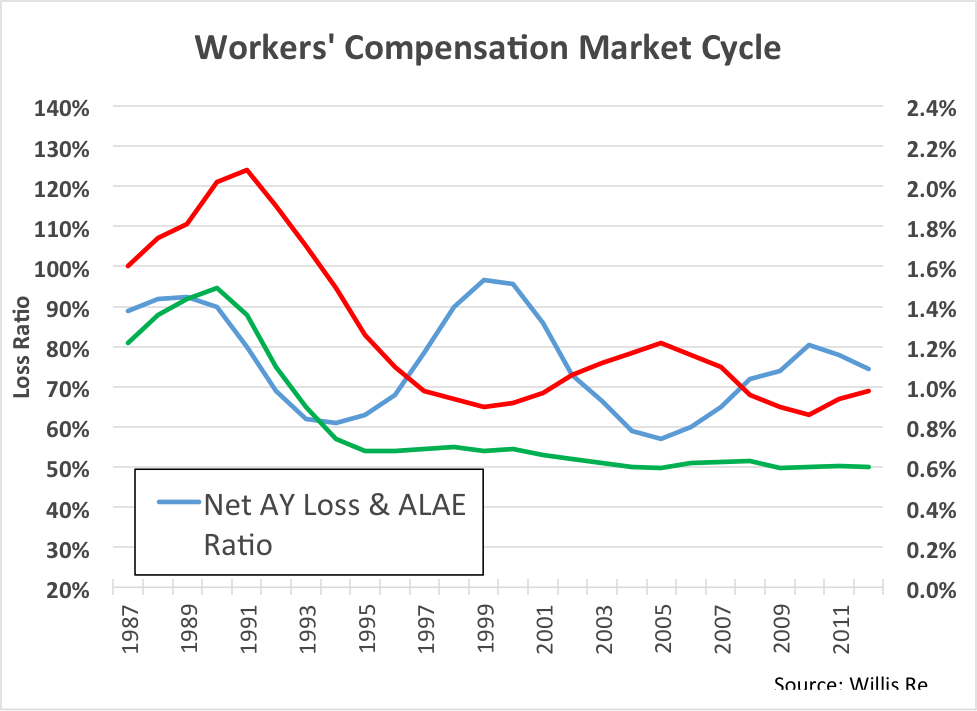

This is an aggregate view of the work comp industry results. The blue line is accident year loss ratio, 1987 to present. See the volatility? Loss ratio is bouncing up and down between 60% and 100%.

Now look at the red line. This is the price line. We see volatility in price, as well, and this makes sense. But what’s the driver here? Is price reacting to loss ratio, or are movements in loss ratio a result of changes in price?

To find the answer, look at the green line. This is the historic loss rate per dollar of payroll. Surprisingly, this line is totally flat from 1995 to the present. In other words, on an aggregate basis, there has been no fundamental change in loss rate for the past 20 years. All of the cycles in the market are the result of just one thing: price movement.

Unfortunately, it appears we have done this to ourselves.

This is an aggregate view of the work comp industry results. The blue line is accident year loss ratio, 1987 to present. See the volatility? Loss ratio is bouncing up and down between 60% and 100%.

Now look at the red line. This is the price line. We see volatility in price, as well, and this makes sense. But what’s the driver here? Is price reacting to loss ratio, or are movements in loss ratio a result of changes in price?

To find the answer, look at the green line. This is the historic loss rate per dollar of payroll. Surprisingly, this line is totally flat from 1995 to the present. In other words, on an aggregate basis, there has been no fundamental change in loss rate for the past 20 years. All of the cycles in the market are the result of just one thing: price movement.

Unfortunately, it appears we have done this to ourselves.

Surprisingly, for carriers using predictive analytics, market cycles present an opportunity to increase profitability, regardless of cycle direction. For the unfortunate carriers not using predictive analytics, the onset of each new cycle phase presents a new threat to portfolio profitability.

Simply accepting that profitability will wax and wane with market cycles isn’t keeping up with the times. Though the length and intensity may change, markets will continue to cycle. Sophisticated carriers know that these cycles present not a threat to profits, but new opportunities for differentiation. Modern approaches to policy acquisition and retention are much more focused on individual risk pricing and selection that incorporate data analytics. The good news is that these data-driven carriers are much more in control of their own destiny, and less subject to market fluctuations as a result.

Surprisingly, for carriers using predictive analytics, market cycles present an opportunity to increase profitability, regardless of cycle direction. For the unfortunate carriers not using predictive analytics, the onset of each new cycle phase presents a new threat to portfolio profitability.

Simply accepting that profitability will wax and wane with market cycles isn’t keeping up with the times. Though the length and intensity may change, markets will continue to cycle. Sophisticated carriers know that these cycles present not a threat to profits, but new opportunities for differentiation. Modern approaches to policy acquisition and retention are much more focused on individual risk pricing and selection that incorporate data analytics. The good news is that these data-driven carriers are much more in control of their own destiny, and less subject to market fluctuations as a result.

What’s Driving the Cycles?

Raj Bohra at Willis Re does great work every year looking at market cycles by line of business. In one of his recent studies, a graph of past workers’ compensation market cycles was particularly intriguing.

This is an aggregate view of the work comp industry results. The blue line is accident year loss ratio, 1987 to present. See the volatility? Loss ratio is bouncing up and down between 60% and 100%.

Now look at the red line. This is the price line. We see volatility in price, as well, and this makes sense. But what’s the driver here? Is price reacting to loss ratio, or are movements in loss ratio a result of changes in price?

To find the answer, look at the green line. This is the historic loss rate per dollar of payroll. Surprisingly, this line is totally flat from 1995 to the present. In other words, on an aggregate basis, there has been no fundamental change in loss rate for the past 20 years. All of the cycles in the market are the result of just one thing: price movement.

Unfortunately, it appears we have done this to ourselves.

Breaking the Cycle

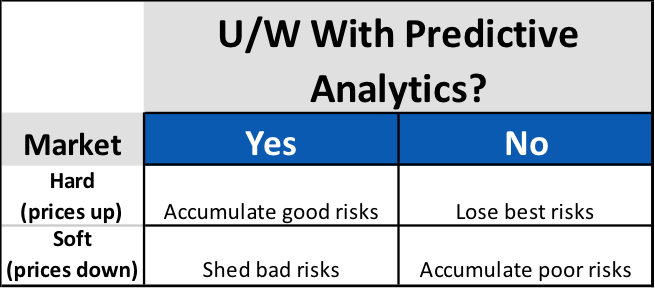

As carriers move to more sophisticated pricing using predictive analytics, can we hope for an end to market cycles? Robert Hartwig, economist and president of the Insurance Information Institute, thinks so. “You’re not going to see the vast swings you did 10 or 15 years ago, where one year it’s up 30% and two years later it’s down 20%,” he says. The reason is that “pricing is basically stable…the industry has gotten just more educated about the risk that they’re pricing.” In other words, Hartwig is telling us that more sophisticated pricing is putting an end to extreme market cycles. The “what goes up must come down” mentality of market cycles is becoming obsolete. We see now that market cycles are fed by pricing inefficiency, and more carriers are making pricing decisions based on individual risks, rather than reacting to broader market trends. Of course, when we use the terms “sophisticated pricing” and “individual risk,” what we’re really talking about is the effective use of predictive analytics in risk selection and pricing.Predictive Analytics – Opportunity and Vulnerability in the Cycle

Market cycles aren’t going to ever truly die. There will still be shock industry events, or changes in trends that will drive price changes. In "the old days," these were the catalysts that got the pendulum to start swinging. With the move to increased usage of predictive analytics, these events will expose the winners and losers when it comes to pricing sophistication. When carriers know what they insure, they can make the rational pricing decisions at the account level, regardless of the price direction in the larger market. In a hard market, when prices are rising, they accumulate the best new business by (correctly) offering them quotes below the market. In a soft market, when prices are declining, they will shed the worst renewal business to their naïve competitors, which are unwittingly offering up unprofitable quotes.

Surprisingly, for carriers using predictive analytics, market cycles present an opportunity to increase profitability, regardless of cycle direction. For the unfortunate carriers not using predictive analytics, the onset of each new cycle phase presents a new threat to portfolio profitability.

Simply accepting that profitability will wax and wane with market cycles isn’t keeping up with the times. Though the length and intensity may change, markets will continue to cycle. Sophisticated carriers know that these cycles present not a threat to profits, but new opportunities for differentiation. Modern approaches to policy acquisition and retention are much more focused on individual risk pricing and selection that incorporate data analytics. The good news is that these data-driven carriers are much more in control of their own destiny, and less subject to market fluctuations as a result.