What if there was a technological advancement so powerful that it transforms the very way the insurance industry operates?

What if there was a technology that could fundamentally alter the way that the economics, the governance systems and the business functions operate in insurance and could change the way the entire industry postulates in terms of trade, ownership and trust?

This technology is here, and it’s called the blockchain, best known as the force that drives Bitcoin.

Bitcoin has gotten a pretty bad rap over the years for good reason. From the collapse of Mt. Gox and the loss of millions – to being the de facto currency for pedophilia peddlers, drug dealers and gun sellers on Silk Road and the darling of the anarcho-capitalist community – Bitcoin is not doing well in the public eye. Its price has also fluctuated wildly, allowing for insane speculation, and, with the majority of Bitcoins being owned by the small group that started promoting it, it ‘s sometimes been compared to a Ponzi scheme.

Vivek Wadhwa writes in the Washington Post that Chinese Bitcoin miners control more than 50% of the currency-creation capacity and are connected to the rest of the Bitcoin ecosystem through the Great Firewall of China, which slows down the entire system because it is the equivalent of a bad hotel Wi-Fi connection. And the control gives the People’s Army a strategic vantage point over a global currency.

Consequently, the Bitcoin brand has been decimated and is thought by too many to be a kind of dodgy currency on the Internet for dodgy people.

The blockchain, a core technology behind what drives Bitcoin, has been slow to enter the Zeitgeist because of this attachment to Bitcoin, the bête noire of the establishment.

But that is changing fast. Blockchain as a tool for disintermediation is simply too powerful to ignore.

People are now beginning to really look at the blockchain as an infrastructure for more than monetary transactions and what it has done for Bitcoin. Just as Bitcoin makes certain financial intermediaries unnecessary, innovations on the blockchain remove the need for gatekeepers from a number of processes, which can really grease the wheels of any business, including insurance companies.

How blockchain works and can work for the insurance industry

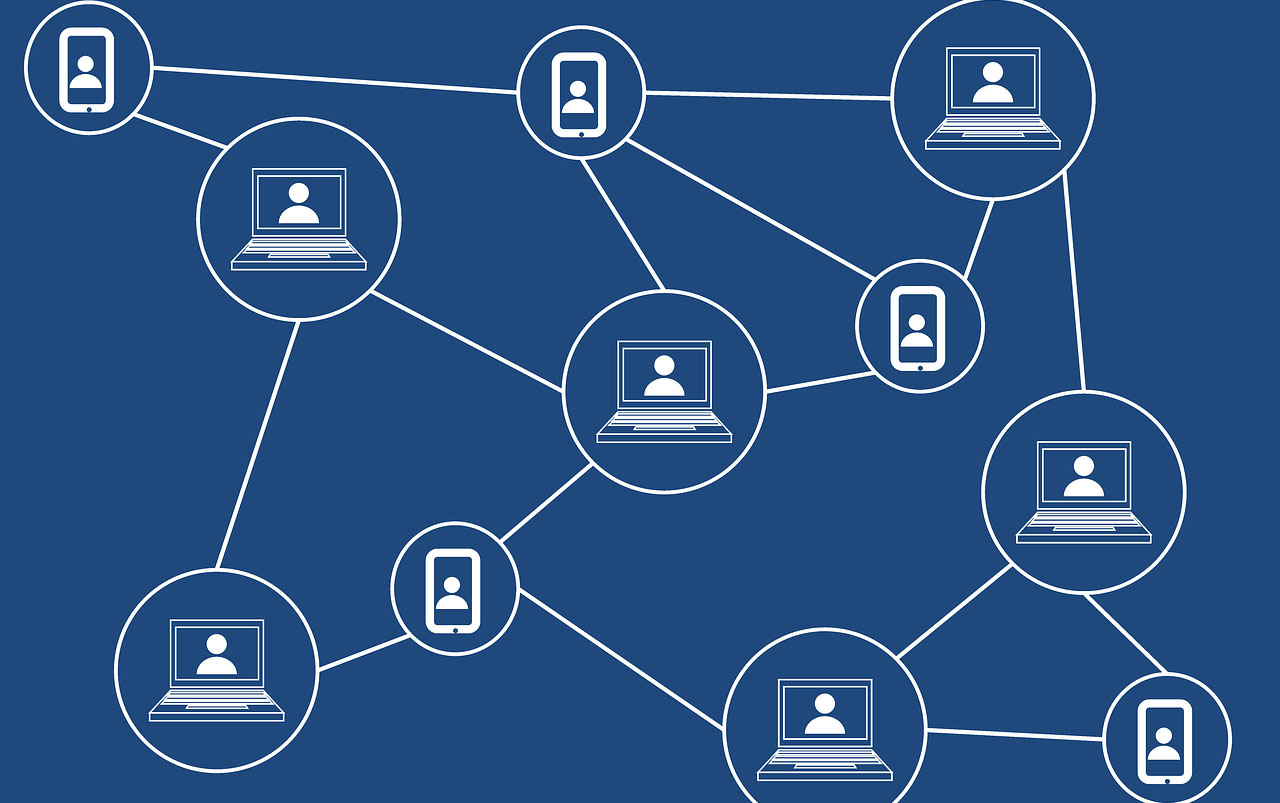

Because of the way it distributes consensus, the blockchain routes around many of the challenges that typically arise with distributed forms of organization and issues such as how to cooperate, scale and collectively invest in shared resources and infrastructures.

In the blockchain, all transactions are logged, including information on the date, time and participants, as well as the amount of every single transaction in an immutable record.

Each trust agent in the network owns a full copy of the blockchain, and, in the case of a private consortium blockchain (more relevant to the insurance industry), the transactions are verified using advanced cryptographic algorithms, and the "Genesis Block" sits within the control of the consortium.

The mathematical principles also ensure that these trust agents automatically and continuously agree about the current state of the blockchain and every transaction in it. If anyone attempts to corrupt a transaction, the trust agents will not arrive at a consensus and therefore will refuse to incorporate the transaction in the blockchain.

Imagine there’s a notary present at each transaction. This way, everyone has access to a shared, single source of truth. This is why we can always trust the blockchain.

Imagine a healthcare insurance policy that can only be used to pay for healthcare at certified parties. In this case, whether someone actually follows the rules is no longer verified in the bureaucratic process afterward. You simply program these rules into the blockchain.

Compliance in advance.

Automation through the use of smart contracts also leads to a considerable decrease in bureaucracy, which can save accountants, controllers and insurance organizations in general an incredible amount of time.

While the global bankers are far out of the blocks when it comes to learning, understanding and now embracing blockchain technology, the insurance industry is lagging. Between 2010 and 2015, a mere 13% of innovation investments by insurers were actually in insurance technology companies.

There are some efforts to tap innovation, as the Financial Times in the UK recently wrote. European insurers such as Axa, Aviva and Allianz, along with MassMutual and American Family in the U.S. and Ping An in Asia are setting up specialist venture capital funds dedicated to investing in start-ups that may be relevant for their core businesses.

Aviva recently announced a "digital garage’ in Singapore, a dedicated space where technical specialists, creative designers and commercial teams explore, develop and test new insurance ideas and services that make financial services more tailored and accessible for customers.

And others are sure to follow in the insurance industry, particularly because both the banking industry and capital markets are bullish on investing in innovation for their own sectors – and particularly because they are doing a lot of investment in and around blockchain.

Still, the bankers and capital markets are currently miles ahead of the insurance industry when it comes to investing in blockchain research and startups.

Competitors in the capital markets and banking industries in terms of blockchain solutions include: the Open Ledger Project, backed by Accenture, ANZ Bank, Cisco, CLS, Credits, Deutsche Börse, Digital Asset Holdings, DTCC, Fujitsu Limited, IC3, IBM, Intel, J.P. Morgan, London Stock Exchange Group, Mitsubishi UFJ Financial Group (MUFG), R3, State Street, SWIFT, VMware and Wells Fargo; and the R3 Blockchain Group, whose members include the likes of Barclays, BBVA, Commonwealth Bank of Australia, Credit Suisse, Goldman Sachs, J.P. Morgan, Royal Bank of Scotland, State Street and UBS.

Then there are start-ups like Ripple and Digital Asset Holdings, led by ex-JPMorgan exec Blythe Masters, who turned down a job as head of Barclays’ investment bank to build her blockchain solution for banking.

There are others in the start-up world moving even faster in the same direction, some actually operating in the market, such as Billoncash in Poland, which is the world’s first blockchain cryptocash backed by fiat currency and which passed through the harsh EU and national regulatory systems with flying colors. Tunisia is replacing its current digital currency eDinar with a blockchain solution via a Swiss startup called Monetas.

There are both threats and opportunities for the bankers... so what about the global insurance industry?

Every insurance company’s core computer system is, at heart, a big, fat centralized transaction ledger, and if the insurance industry does not begin to learn about, evaluate, build with and eventually embrace blockchain technology, the industry will leave itself naked and open to the next Uber, Netflix, AirBnB or wanna-be unicorn that comes along and disrupts the space completely.

Blockchain more than deserves to be evaluated by insurers as a potential replacement for today’s central database model.

Where should the insurance industry start?

Companies need to start to experiment, like the bankers and stock markets, by not only working with existing blockchain technologies out there but by beginning to experiment within their own organizations. They need to work with blockchain-focused accelerators and incubators like outlierventures.io in the UK or Digital Currency Group in the U.S. and tap into the latest start-ups and technologies. They need to think about running hackathons and start to build developer communities – to start thinking about crowdsourcing innovation rather than trying to do everything in-house.

Apple, Google, Facebook and Twitter have hundreds of thousands of innovators creating products on spec via their massive developer communities. Insurance companies that don’t start lowering their walls might very well find themselves unable to innovate as quickly as emerging companies that embrace more open models in the future and therefore find themselves moot. Kodak meet Instagram.

The first step for insurance companies with blockchain technology will likely be to look at smart contracts, followed by looking for identity validation and building new structural mechanisms where parties no longer need to know or trust each other to participate in exchanges of value.

Blockchain technology, for instance, can also allow for accident or health records to be stored and recorded in a decentralized way, which can open the door for insurance companies to reduce friction in the current systems in which they operate.

Currently, the industry is highly centralized, and the introduction of new blockchain-fueled structures such as mutual insurance and peer-to-peer models based on the blockchain could fundamentally affect the status quo.

As comedian and writer Dominic Frisby once penned, "The revolution will not be televised. It will be cryptographically time stamped on the blockchain."

Some of the many questions that the industry should explore:

- What kind of effect will blockchain technology adoption in markets have on the the public’s perception of risk?

- Today, the insurance industry is centralized, but what could it look like if it were decentralized?

- How could that affect how insurance companies mutualize?

- Can the blockchain improve customer relations and confidence?

- Can smart contracts built on the blockchain automate parts of the process in how business is done in the insurance industry?