The integration of technology in the insurance company’s value proposition is turning out to be one of the main evolutionary trends in the sector, and digital initiatives have been for a couple of years now one of the priorities of insurance groups. Until today, though, they have brought only limited improvement when it comes to the competitive abilities of the insurer.

The best practices at the international level show that, to obtain concrete benefits, the innovation has to be directed toward clearly determined strategic objectives.

An interesting example is the American company Oscar – a start-up that in less than two years has managed to raise more than $300 million at a valuation of more than $1.5 billion. It has radically innovated the customer experience of individual health insurance policies by directing the innovation effort toward two key factors that are crucial for the profitability of the medical spending reimbursement business: deductibles and “emergency” visits.

Oscar has created an insurance value proposition based on a smartphone app that incorporates a highly advanced search engine – including a search based on symptoms – allowing the insured to identify and compare the medical structures part of the preferred network. In this way, the client receives support in optimizing direct spending before reaching the deductible; this basically postpones when the insurance company starts to pay and thus reduces the amount of spending (medical reimbursements) by the insurer for the remainder of the year.

The company addresses emergency visits by providing chat with a specialist and a call-back system that the insured can choose at will from inside the network. This represents a comfortable alternative and reduces the number of urgent visits.

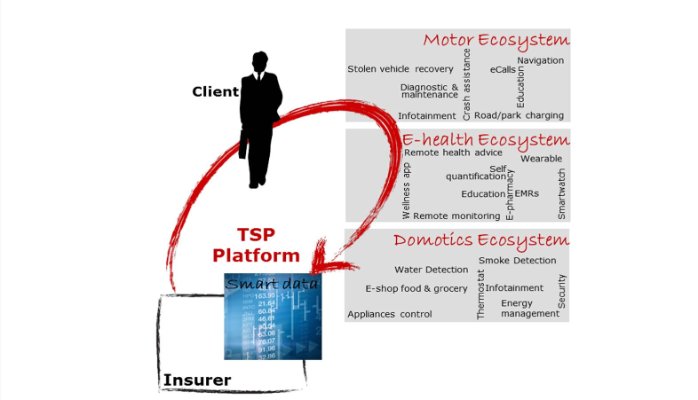

Health insurance and connected health

In these last months, I have been considering how to replicate the motor telematics experience for the health insurance sector. Insurance companies see the benefits from a telematics black box and how the return on investment in this type of technology can be maximized by the insurer: This is possible by taking into consideration not only the underwriting of the car insurance policy but by also looking at the services provided to the client, at loss control and at customer loyalty. In health insurance, similar benefits are achievable by using mHealth devices and wearables.

The first element is risk selection, seen in car insurance as:

- the capacity of auto selection and dissuasion of risky behavior,

- the integration of static variables traditionally used for pricing with a set of “telematics data” gathered within a limited time and used exclusively for supporting the underwriting phase.

- commercial appeal

- capacity to acquire less risky clients

- ability to gradually reduce the risk profile of the single client.