Life insurers base their business on anticipating and accounting for catastrophic mortality events, including natural disasters, war, accidents and disease. The COVID-19 pandemic presented a unique opportunity: It allowed life insurers to evaluate how well they anticipated the effects of a global pandemic and study COVID’s actual impact to adjust their modeling for future pandemics.

Insurers can look back much further than COVID-19 for valuable insights into the mortality and morbidity outcomes of pandemics, including the devastating effects of the 1918 Spanish flu, the deadliest pandemic in the last 400 years. While researchers anticipate an increasing frequency of extreme epidemic events, numerous factors affect the spread and penetration of diseases across global populations. By isolating these factors and studying them in combination, life insurers can better prepare for future disease outbreaks.

While the terms are sometimes used interchangeably, pandemics and epidemics are distinct. An epidemic is a disease outbreak that occurs within a specific geographical area. A pandemic occurs if the disease spreads to multiple areas or the entire globe.

The chance of a pandemic occurring depends on the combined effects of two factors: spark risk (how and where a pandemic is likely to start) and spread risk (how easily the resulting disease can transmit between people). Spark and spread risk factors often overlap.

See also: Is 2024 the Year of Digital Health?

Some geographic areas are associated with a higher spark risk. For example, West and Central Africa and South and Southeast Asia, areas of increasing human expansion into animal habitats, carry higher risk for zoonotic spark, where a viral pathogen jumps from animals to humans.

Risk drivers for a zoonotic spark include:

- Behavioral factors, such as bushmeat hunting and use of animal-based traditional medicines

- Natural resource extraction, such as logging, mining and the retrieval of fossil fuels

- Extension of roads into wildlife habitats, increasing interactions between humans and animals

- Environmental factors, including the degree and distribution of animal diversity (For example, the high number of zoonotic viruses found in bats and birds has been attributed to their large populations, mobility, ability to colonize human environments and significant species diversity.)

Zoonoses (diseases that move from animals to humans) can also originate from domesticated animals, particularly those concentrated in areas with dense livestock production systems, including areas of China, India, Japan, the U.S. and Western Europe.

Zoonoses are not well adapted to infect humans. They typically spill over to people in random incidents, sometimes resulting in small, contained outbreaks referred to as stuttering chains. These instances of intermittent virus transmission, or "viral chatter," raise the threat of a pandemic because they give viruses opportunities to evolve and more effectively spread among humans.

Spread risk encapsulates the transmissibility of a virus and its variants. After a spark, the risk that a pathogen will spread within a population is influenced by:

- Pathogen-specific factors (such as its R0, discussed later in this article)

- Human population-level factors (such as the density of the population, and the speed and effectiveness of public health surveillance and response measures)

A country’s ability to minimize pandemic spread can be expressed using a preparedness index. The index illustrates global variation in institutional readiness to detect and respond to a large-scale outbreak of infectious disease.

See also: The Crisis in Long-Term Care

Well-prepared countries have effective public institutions, strong economies and adequate investment in their health sectors. They have built specific competencies critical to detecting and managing disease outbreaks, including surveillance, mass vaccination and risk communications. Poorly prepared countries may suffer from political instability, weak public administration, inadequate resources for public health and gaps in fundamental outbreak detection and response systems.

The COVID-19 pandemic illuminated the fact that our global community is facing the greatest confluence of spark and spread risk factors compared with any point in history. Today’s global population is over four times larger than it was at the time of the 1918 influenza pandemic. We live more densely and travel frequently. Experts suggest that these trends and those outlined above have dramatically increased, and will continue to increase, the emergence of zoonotic diseases.

Historic pandemics and the shadow of the Spanish flu

Despite the seemingly unprecedented panic and worldwide disruptions caused by COVID-19, pandemics are nothing new. The emergence and spread of infectious diseases with pandemic potential – such as plague, cholera, tuberculosis and influenza – have occurred regularly since the dawn of mankind.

Before SARS-CoV-2 emerged in late 2019, most of the infectious disease research community anticipated that the most likely pathogen to cause the next pandemic would be a novel influenza strain. The human-adapted influenza virus transmits easily from person to person; people can carry it without showing symptoms, allowing sufficient time for infected individuals to travel and potentially infect others; and its symptoms can be confusing and difficult to immediately identify as the flu, particularly in the early periods of infection.

These deadly attributes fed the astonishing progression and spread of the 1918 Spanish flu, which killed between 20 million and 100 million people at a time when the global population was just 1.8 billion.

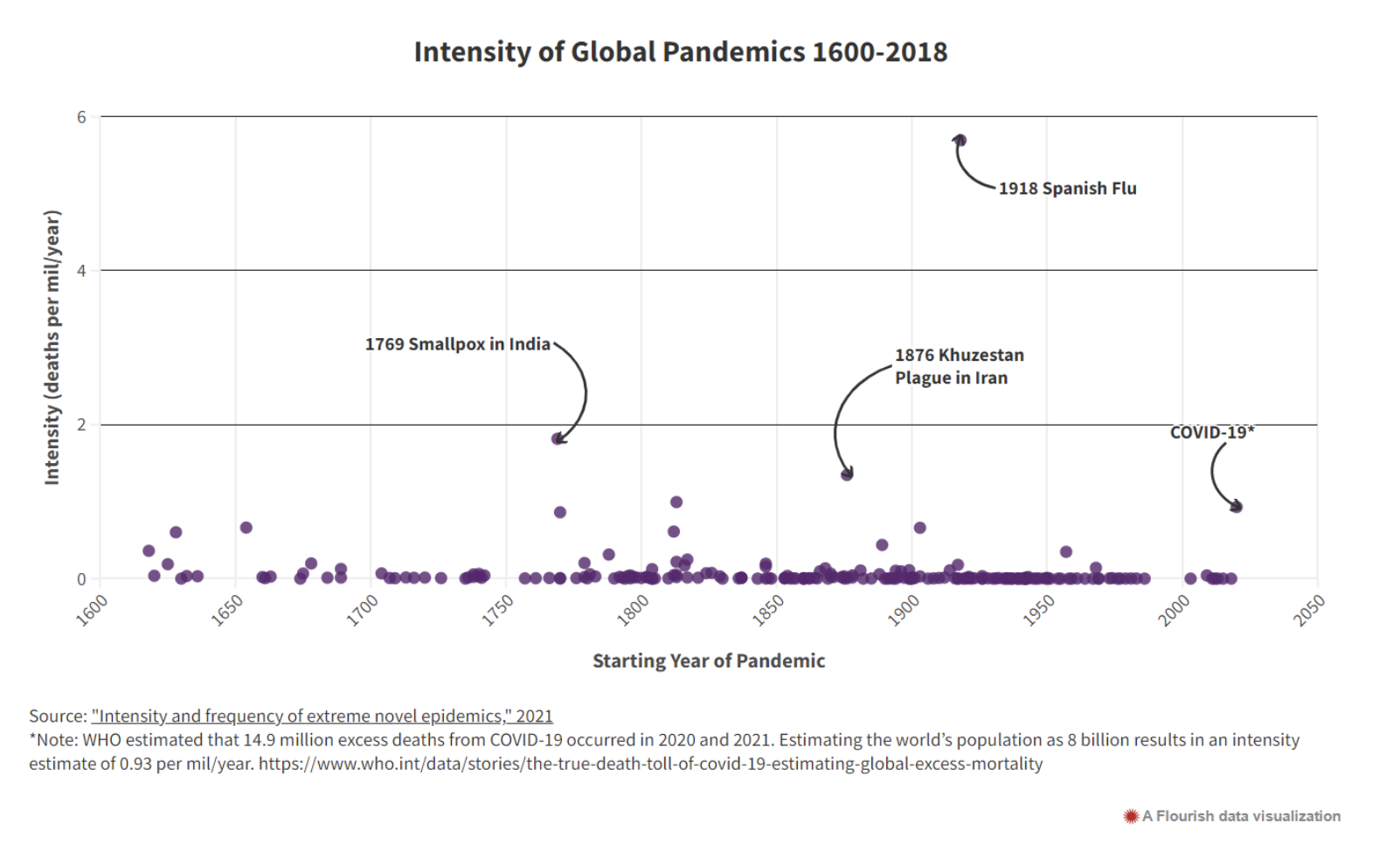

In August 2021, a group of environmental engineering researchers led by Marco Marani published a paper on the “Intensity and spread of extreme novel epidemics.” They combed 400 years of records to identify 185 pandemics globally that caused significant loss of human life. While COVID-19 upended our global society for a time, that pandemic's impact (and that of nearly every other pandemic on record) is dwarfed by the devastation wrought by the 1918 Spanish flu.

This chart illustrates pandemic intensity, defined as the number of deaths divided by the global population at that time and the pandemic's duration – essentially, deaths per 1,000 people per year. The researchers examined the probability of humans experiencing a pandemic as severe as the Spanish flu. Assuming risk is stationary, they estimated that the probability of such a pandemic occurring yearly is 0.42%. Put another way, a pandemic of such an extreme scale would occur once every 235 years.

What made the Spanish flu deadly? Primarily its lethality and transmissibility.

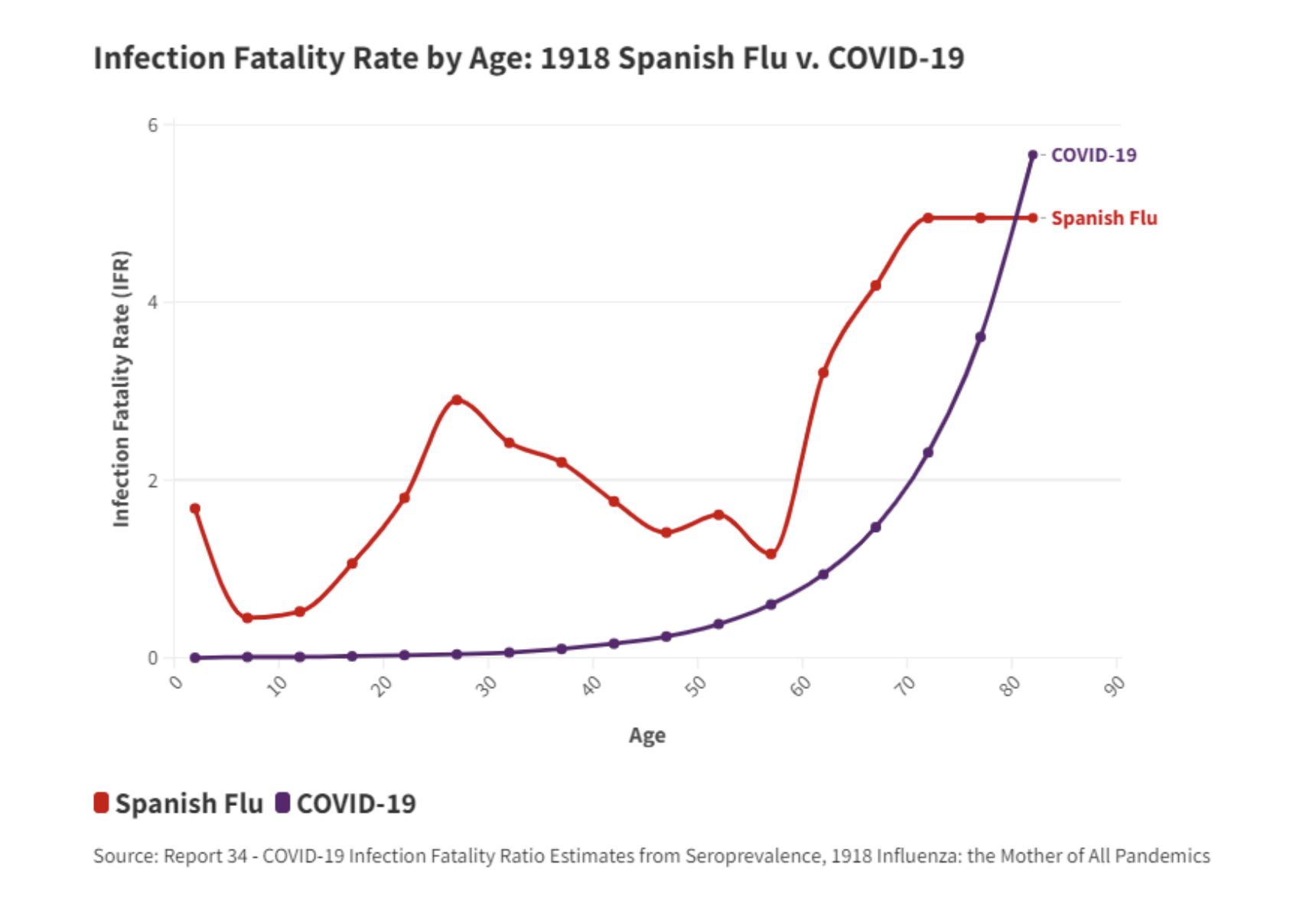

Infection fatality rate (IFR): Spanish flu uniquely affected working-age people in their 20s and 30s. When plotting the IFR by age, researchers expect to see a “U” or “J” among the data points for most viruses: The youngest and oldest lives are those with the greatest risk. The 1918 Spanish flu instead presents a remarkable “W” shape, demonstrating how deadly the virus was to a normally robust working-age population.

The overall IFR for Spanish Flu was 2.2% using a present-day age pyramid of the U.S. population. To put that in context, some estimates suggest the original strain of COVID-19 carried 0.8% IFR. Later variants of COVID-19 carried higher and lower IFRs; the Delta strain of COVID perhaps had an IFR very close to 2.2% and, like Spanish flu, seemed to be more lethal to working-age people.

Spread/R0: Pronounced “R naught,” R0 is a mathematical term that indicates the average number of people who will contract a contagious disease from one person with that disease. R0 is a function of numerous biological, socio-behavioral and environmental factors: for example, population density and patterns of social interactions, work and travel. R0 is a fundamental calculation that helps researchers estimate the spread of a pandemic and the effectiveness of interventions like quarantine, masking and vaccines.

Scant epidemiological data make it difficult to estimate the R0 of the Spanish flu, which circled the globe with spectacular effectiveness given limited means of travel at the turn of the century. One study estimated its R0 to be 1.7-2. Interestingly, Spanish flu was generally less transmissible than COVID-19. The original strain of COVID-19 carried an R0 of approximately 2.5; later strains like Delta (R0 estimated 6) and Omicron (R0 estimated 8) were much more transmissible.

Could a Spanish flu-level pandemic occur today? In 1918, many U.S. cities attempted non-pharmaceutical interventions (NPIs) such as isolation, quarantine, use of disinfectants and limits on public gatherings to curb the pandemic. But without modern medicine, including antibiotics, flu vaccines and antiviral drugs – and compounded by poor sanitation and food scarcity caused by World War I – Spanish flu ravaged the global population. Today’s world is much better equipped to respond to an influenza pandemic. One model from 2018 estimated that nearly 70% fewer deaths would result from a Spanish flu event had it occurred 100 years later.

Assessing the risk of future pandemics

To estimate the frequency and severity of future pandemics, researchers employ probabilistic modeling techniques that can augment the historical record with a large catalog of hypothetical, scientifically plausible simulated pandemics that represent a wide range of possible scenarios.

Modeling can also incorporate significant changes that have occurred since historical times, such as medical advances, changing demographics and shifting travel patterns.

Researchers can “play” with their models by applying different rates of IFR and R0 to gauge the impact of a simulated pandemic. Other key modeling assumptions might include the choice and effectiveness of NPIs, the timing of a vaccine rollout, vaccine efficacy and uptake.

These exercises are essential for assessing risk. A 2020 report from the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) warns that future pandemics will emerge more often, spread more rapidly, do more damage to the world economy and kill more people than COVID-19 unless there is a transformation in the global approach to dealing with infectious diseases, from reaction to prevention.

See also: Growing Number of Uninsurable Risks

Lessons learned from COVID-19

Given the high probability of future pandemics, the most recent global pandemic offers key lessons for insurers and policymakers.

Vaccines: Vaccines do not solve everything, and herd immunity – when a large portion of a community (the herd) becomes immune to a disease – may be difficult or impossible to achieve. Developing, manufacturing and distributing vaccines – a process that itself took months to complete – helped immensely in protecting public health, but COVID-19 and its deadly variants continued to spread even after wide introduction of vaccines. Additionally, no vaccine is 100% effective. Public health officials also realized not every person is willing to take a vaccine. Vaccine hesitancy varies considerably by age, country and other factors – although vaccine uptake is markedly higher in insured lives. As early as 2019, the World Health Organization (WHO) named vaccine hesitancy as one of the top 10 threats to global health.

Ripple effects: COVID-19 deaths were not the only driver of excess deaths during the pandemic. In addition to causing economic shocks, the pandemic overwhelmed health systems, causing significant delays in treatments for other medical conditions. The pandemic also influenced other public-health problems, exacerbating addiction-related deaths, mental illness and anxiety disorders and financial stress and housing insecurity.

Country differences: During the pandemic, researchers observed that infection and mortality rates differed between countries based on several risk factors. RGA researchers conducted a correlation analysis and found the following drivers had the highest correlation to COVID-19 deaths globally:

Prevalence of cardiovascular diseases

Gross domestic product (GDP)

Gini index (income inequality)

Vaccine uptake of the first two shots

Proportion of population living in urban areas

RGA researchers studied other risk factors like obesity and smoking but did not find a strong enough correlation for those factors.

Differences between the insured and general population: In general, the mortality on fully underwritten products is significantly lower than that of the general population, because full medical underwriting usually removes at‐risk groups, such as people with underlying chronic diseases. Insured individuals tend to have a higher socioeconomic status, which may afford them better healthcare access and greater awareness of pandemic risks. However, this same demographic is more prone to travel internationally and reside in densely populated urban centers, factors that can introduce different risks.

RGA research, including a series of COVID mortality reports and updates written with the Society of Actuaries (SOA) and LIMRA, determined the direct and indirect impact COVID-19 has had on mortality in insured lives as well as the general population. It was clear from these studies that COVID-19 levied unequal effects on mortality rates in insured lives versus the general population, with significant differences by age, also.

Conclusion

The experiences of the COVID-19 pandemic, set against the backdrop of historical contagions like the Spanish flu, offer an invaluable learning opportunity for life insurers and life reinsurers to reassess their exposure to catastrophic mortality events. While the probability of a pandemic in any given year is low, the likelihood of significant losses for insurers is high without adequate risk management. Life insurers can take this opportunity to refine their internal risk models as well as their risk management strategies.

Some strategies to consider include reinsurance, and pursuing a diversified product range and geographical footprint. Other risk mitigation strategies include asset choice and management, and insurance‐linked securities (such as catastrophic mortality bonds).

The constant exposure of life insurers to pandemic risk remains a challenging issue; however, the COVID-19 pandemic has certainly deepened our understanding of this risk. Furthermore, pandemic preparedness and health security are now even more critical matters for governments, public health organizations and other institutions around the globe.