Until recently, traditional methods of assessing and financing natural perils have worked well, but conditions have changed. Extreme weather and climate events are increasing in frequency and severity, while value at risk is growing exponentially. Historical underwriting and portfolio management approaches are no longer sustainable for insurers. To keep insurance available tomorrow, innovation is required today.

Insurance plays a critical role in resilience. The billions of dollars insurers pay out in claims annually enable policyholders to rebuild their lives and livelihoods. But what happens when insurers can no longer offer protection due to accumulated losses, restrictive state regulations, or a lack of reinsurance capital to transfer risk?

See also: Insurers Must Evolve to Survive Climate Crisis

Individuals, businesses and communities struggle. Some organizations suffer uninsured losses and are forced to close their doors. Local and regional economies slow. The financial fallout affects many.

Southern California has suffered from two of the most destructive wildfires in state history. The Palisades and Eaton fires, which started in early January, have claimed at least two dozen lives and consumed 40,000 acres of homes, businesses and landmarks, with estimated economic losses of $250 billion, according to the Los Angeles Times. As property owners and government officials survey the devastation, insurance companies are facing angry questions about why many are not renewing policies and withdrawing from underwriting risks in the state.

California's insurance regulatory system has had an impact, but it's not the whole story. To continue offering protection in a state with a long history of wildfires, insurers need ways to accurately and sustainably underwrite a risk that is evolving rapidly.

Severe convective storms (SCS) — while not the most attention-grabbing — are actually the most destructive peril, with Aon reporting insured SCS losses totaled $61 billion last year, making it the costliest peril for insurers. Not only are they becoming more frequent but they also pose an existential threat to insurance companies. In 2023, SCS losses were responsible for the insolvencies of four insurers and rating downgrades for dozens of others.

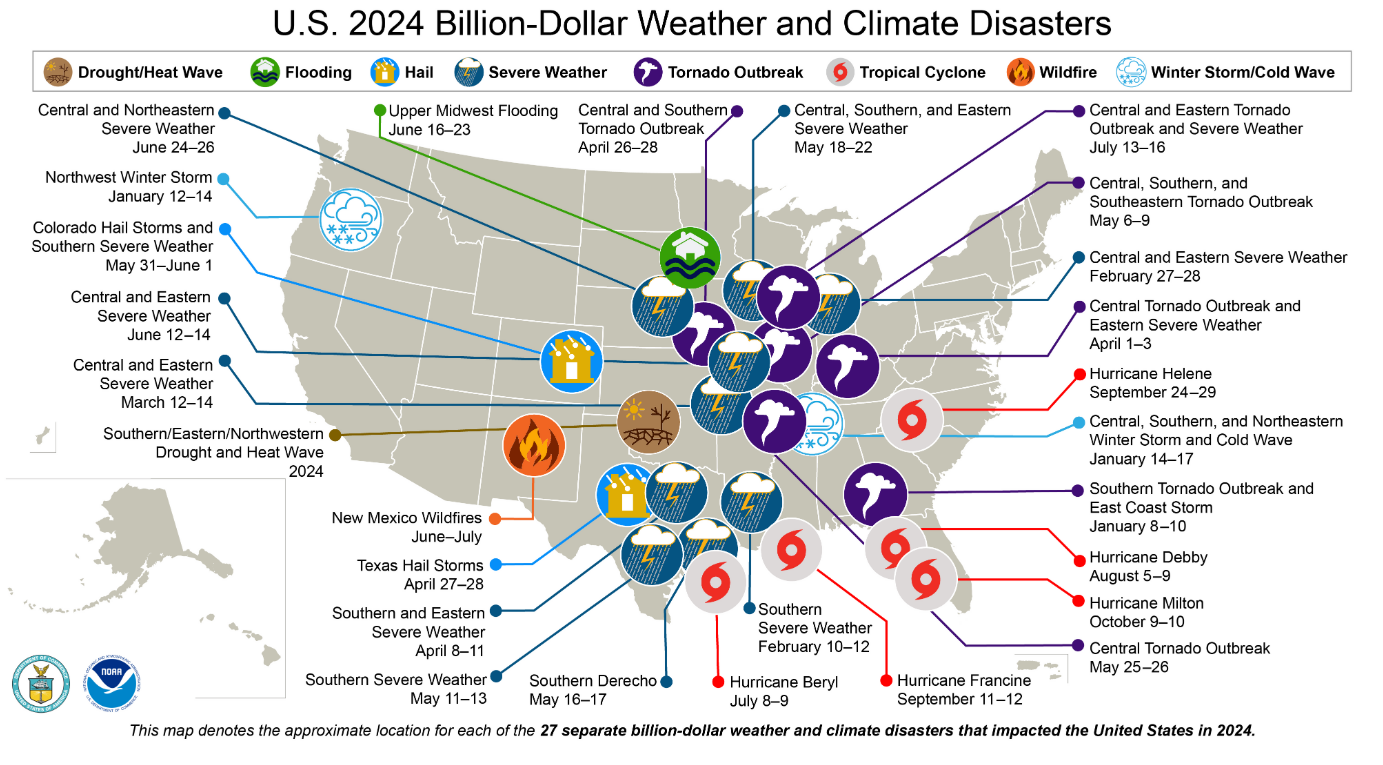

In 2024, the National Oceanic and Atmospheric Administration (NOAA) reported 27 weather and climate disasters that each caused more than $1 billion in damage. 17 involved tornadoes, hail or severe thunderstorms. Less than one-fifth of the billion-dollar disasters NOAA tracked in 2024 were tropical cyclones. Between 1980 and 2024, the annual average of billion-dollar events is nine. In 2020-2024, however, that number rose to 23. More of the U.S. is experiencing severe storms, and insurers are paying more for the losses those events cause.

The problem with SCS loss frequency and severity is insurers are unable to spread this risk through traditional catastrophe reinsurance programs. Reinsurers have been reluctant to provide aggregate loss coverage, and even though limited protection was briefly available years ago, it was cost-prohibitive for insurers. As a result, insurers today can reinsure hurricane risks but must retain SCS losses on their balance sheets. With limited options for spreading risk, insurance companies eventually must decide when the aggregation of claims forces them to curtail their underwriting where SCS perils are present. That is simply not sustainable.

Keys to financial stability

Insurance as a business relies on several conditions to exist. The first of those is a clear understanding of the risks that insurance companies assume on their balance sheets. Next is the ability to accurately price those risks. Third is the ability to spread risks — within a portfolio of policies and with access to reinsurance capital. When these three conditions exist, the result is financial stability, with adequate surplus and capital to pay claims.

Claims ebb and flow from year to year, but unless insurance companies can absorb those losses and underwrite risks profitably, they cannot remain in business — or continue to offer policies for those risks. That ultimately means additional financial burdens for taxpayers.

Sustainability is a major challenge for all businesses, and it's especially acute in insurance. The benefits of a stable, sustainable insurance industry are many — financial protection remains accessible, funds are available when losses strike, and local economies can continue growing.

See also: Insurers Face Complex Risk Environment in 2025

Innovation to mitigate risks

Amid current trends, secondary perils such as wildfires and severe convective storms are driving financial volatility for insurers and policyholders. To mitigate these risks and keep insurance available in geographies where such perils threaten life and property, the insurance industry needs to embrace innovation.

Innovation is already occurring in modeling risks and losses, producing significant improvements in evaluating and pricing risks. Novel risk transfer solutions also exist, including parametric modeled-loss policies that provide cost-effective reinsurance of secondary perils. With these enhanced tools, perils that some insurers have opted to avoid can be insured.

History offers some lessons for insurance policyholders and policymakers. In the past, when risks became too frequent and severe for the insurance industry to handle, the industry called for a federal solution. This has occurred multiple times in the past century — flooding and homeowners insurance led to the National Flood Insurance Program in 1968, the Sept. 11, 2001, terrorist attacks and terrorism risk resulted in the Terrorism Risk Insurance Act in 2002, a federal backstop for systemic cyber risk is still being debated.

Are wildfires and severe convective storms next on the list of risks that require government funding? The private insurance industry appears to have adequate capital to underwrite these risks, with better tools for risk assessment and risk transfer. These innovations can keep insurance available where individuals and businesses most need the protection it offers.