At one time, life seemed to be compartmentalized. Work was work. Home was home. You commuted to work or business. Your work stayed at work. You slept and ate at home. You might drive back out to a movie or a restaurant on the weekend. With the exception of agricultural jobs, where home and farm were often the same, most of us lived and operated within these compartments. Insurers understood the compartments and insured them appropriately. Insurers and their agent channels knew how to catch us where we would be most likely to sign up for insurance. They were adept at selling.

Convenience and technology, however, kept creeping into the picture. We had our newspapers and mail delivered to our homes but now receive them digitally. We watched movies at the mail but now download or stream them. We had pizza delivered and now can have nearly any restaurant food or groceries delivered. We ordered books online with a click and now can download them to read on tablets.

This trickle of ease and use of technology gave us a taste of how convenience could improve our lives. Aspects of our compartments were seeping into the other compartments. This made selling a more difficult process. All industries had to rethink their products and services from the standpoint of the customer – their desire for convenience and use of technology. If you couldn’t get people to go to their entertainment, you had to bring it directly to their homes. If you couldn’t get people to walk into your bank, you needed to place your bank on their phones.

We are now evolving beyond convenience. Life is no longer compartmentalized. It has gotten complicated. Customers want simplification and a holistic view to manage their lives across many different areas. And insurers have to pay attention to the changes. What happens when a large portion of the population begins to drive their cars for work instead of to work or many people shift to work at home instead of working “at work”? What if people want value-added services to manage risk – from their homes and autos to their health and more? These are radical shifts that are rewriting the stories of insurance. The nature of home, work, business and family are erasing the conceptual lines that kept insurance “traditional.”

In this blog, we are going to give you a high-level peek at some of the trends we found in our annual consumer survey. Some of them will make you want to press fast-forward on your strategic plans. Others may cause you to rethink how your organization fits within other ecosystems that customers want and are willing to buy insurance from. No matter what you find, you’ll be better-informed as you grapple with important decisions and future plans.

The Gen Z and Millennial Lens

Though Majesco’s report covers all age groups, insurers that are concerned about the near future will be most interested in the shifts and interests among Gen Z and Millennials. They are now the dominant buyers for both life and non-life insurance products, with a focus on five segments: life/health/accident, employee/voluntary benefits, auto, mobility and homeowners/renters insurance.

Millennial and Gen Z life journeys have not followed the traditional path set by older generations, with high percentages remaining single and not married but with partners. They have made other significant lifestyle shifts from older generations that result in different risk needs that require different insurance needs.

Over the next three years, Gen Z and Millennials plan to accelerate their life journeys through rapid change, outpacing the older generation in all aspects, including twice the average rate of changes in the home, work and mobility aspects of their lives.

These shifts align with a shift in expectations regarding the types of insurance products they need, the necessity for value-added services and the demand for personalized underwriting. This will pressure insurers to accelerate and improve IoT and data strategies.

The Millennial and Gen Z populations desire a holistic customer experience – where digital offerings bring together other products and services to help customers manage their lives. This necessitates a full view for customers across their insurance products, value-added services and non-insurance products. When insurers can’t deliver that view, a gap arises between customer expectations and what insurers are delivering. This gap opens the door for new competitors to meet that expectation – either directly or through partnerships with insurers. Just consider what companies like Toyota, Sofi, Ford, Petco and Outdoorsy are doing by offering insurance products through embedding or partnering on channel options with various insurers. This year’s research adds clarity to the market areas where insurers are currently missing opportunities.

CAUTION: Opportunities Ahead

If change brings opportunity, then insurers are right now staring at an ocean of real opportunities. Let’s look at the changes that are most prominent.

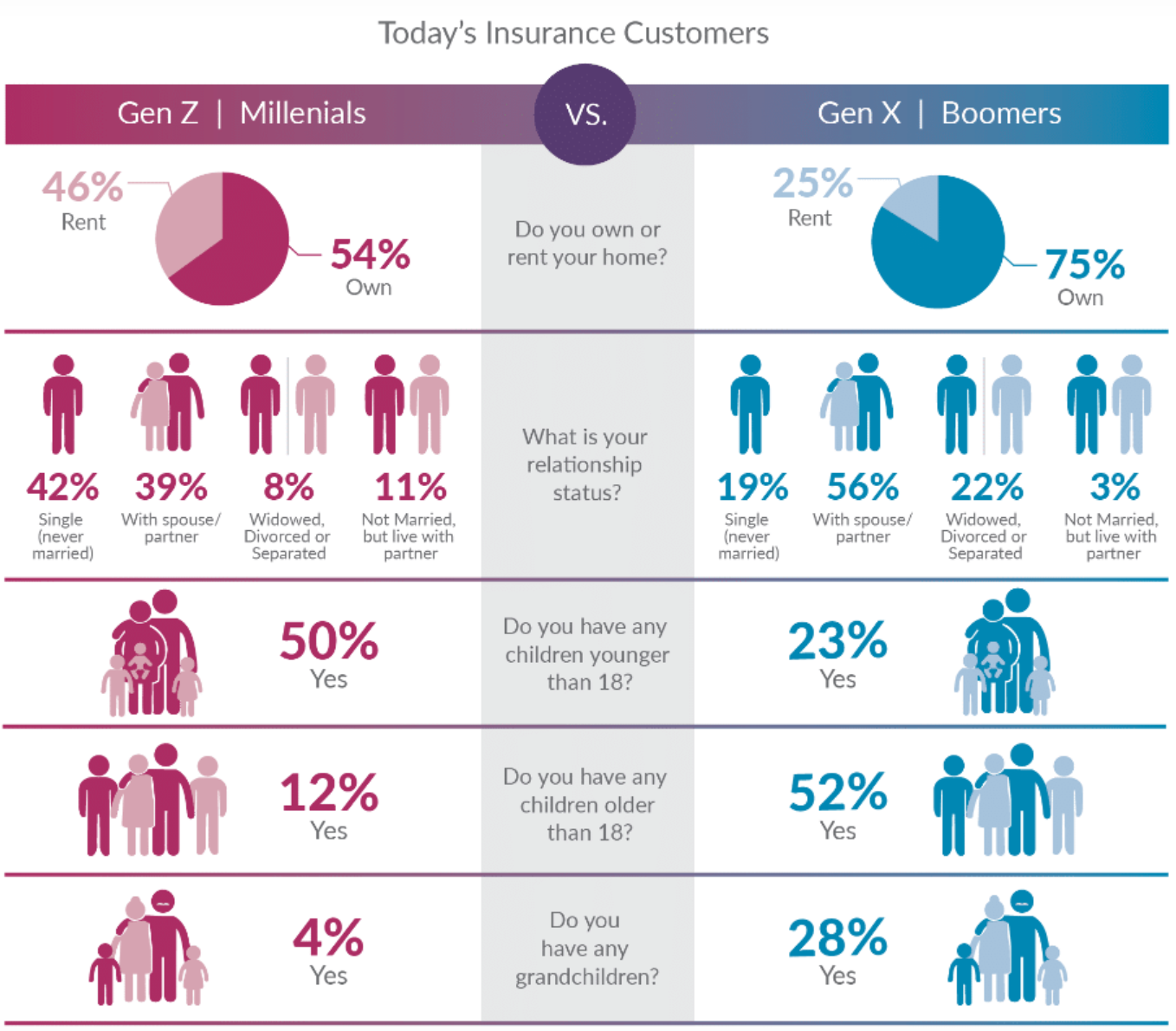

Millennials’ life journeys have not followed a traditional path, largely due to the severe economic stress of the 2007-2009 Great Recession as they entered the workforce. Since then, many have achieved a firm foothold in their life journeys, with a growing majority owning their homes and having children. Yet, high percentages of Gen Z and Millennials are single (42%) and not married but with partner (11%), reflecting a significant lifestyle shift from older generations, which likewise reflects different insurance needs as seen in Figure 1.

Figure 1: Life stage characteristics of today's insurance customers

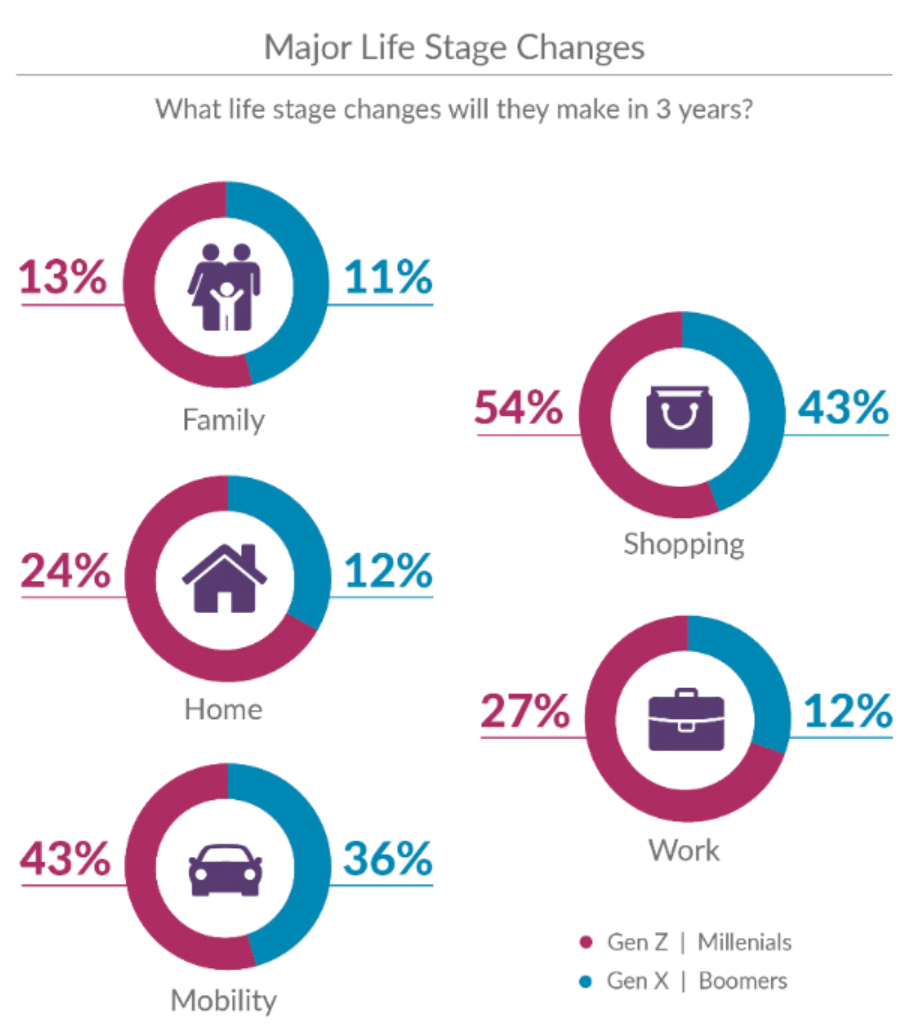

Over the next three years, Gen Z and Millennials will outpace Gen X and Boomers in lifestyle changes in all aspects, including twice the average rate in home and work categories, as seen in Figure 2. Each of these aspects is assessed in detail in the report over the seven-year window.

Figure 2: Expected life stage changes in the next three years

Every area that directly affects the need for and use of insurance is prime for growth. The only question is whether insurers are prepared to capitalize on that growth. In many cases, the growth won’t be through traditional methods of selling or even through traditional products. Digital plays a HUGE role in their expectations. And holistic lifestyles and the desire for convenience will push insurers to digitize and innovate their channel and ecosystem partners to place their products at the point of life events and important larger purchases.

COVID-19 Hastens Market Shifts by Making Insurance Top-of-Mind

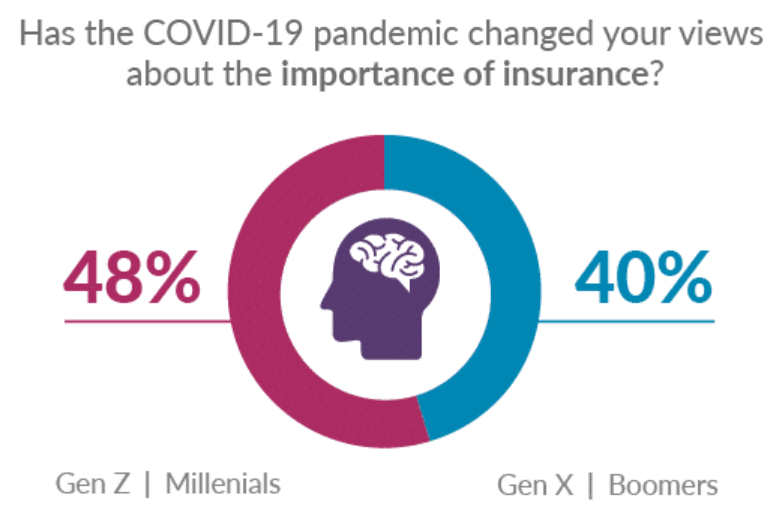

A connected facet of insurance’s potential growth and change is a new protective mindset. A crucial factor influencing all generations is COVID-19 and customers’ views on insurance. Nearly half of Gen Z and Millennials and 40% of Gen X and Boomers in this year’s research felt that insurance has become more important due to the pandemic. (See Figure 3.)

Figure 3: COVID's impact on the importance of insurance

Is “the COVID Effect” a fad? Possibly, but unlikely. Even if COVID were to evaporate overnight, general uncertainty over new weather patterns, social and political unrest and property investments means that insurers need to respond quickly with new or modified products, value-added services and customer experiences that meet rapidly changing customer needs and expectations. The work and home trends that were accelerated by COVID have been around long enough to have made a lasting impression on both the economy and consumer sentiment.

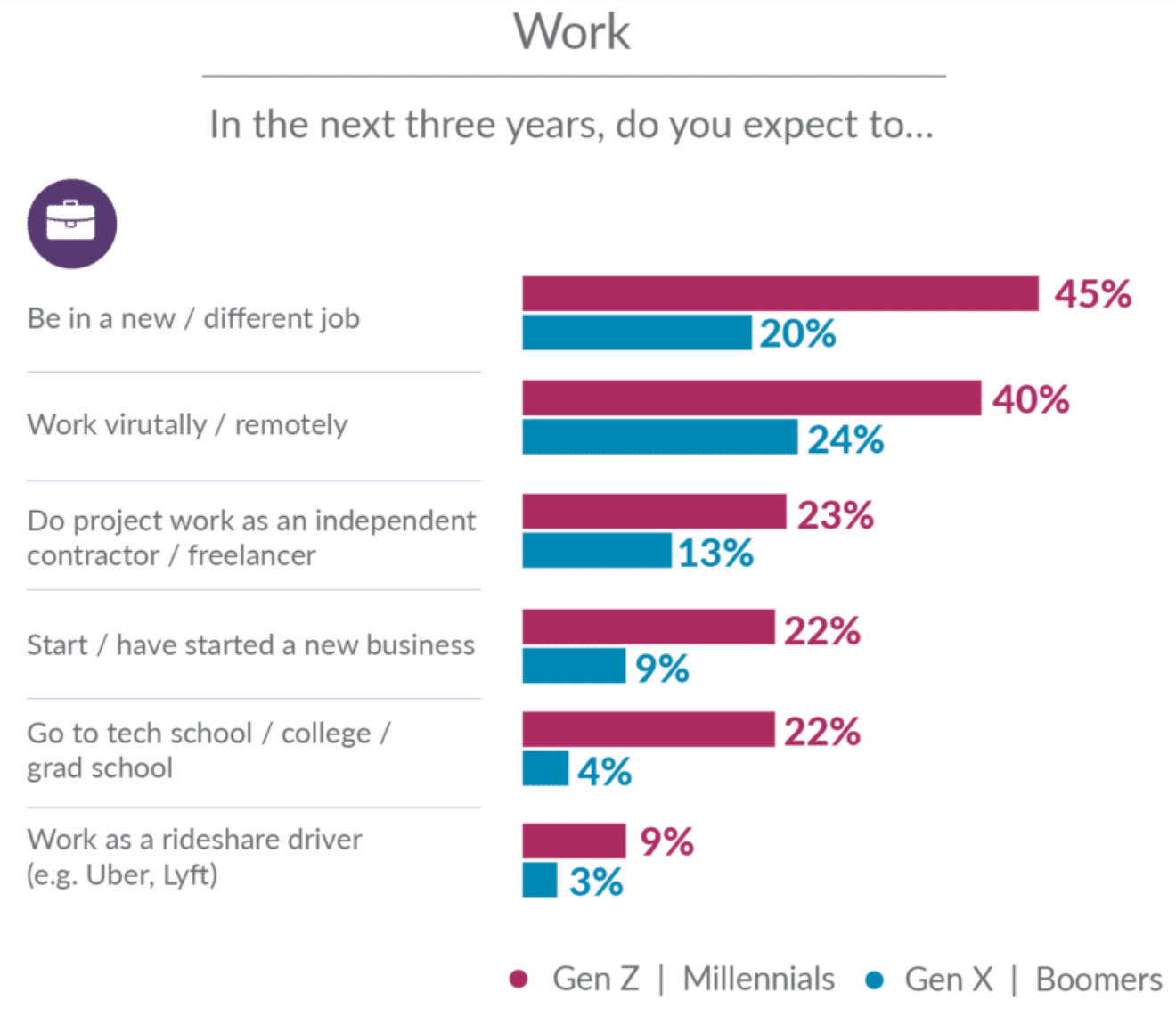

Opportunities in the Widening World of Work

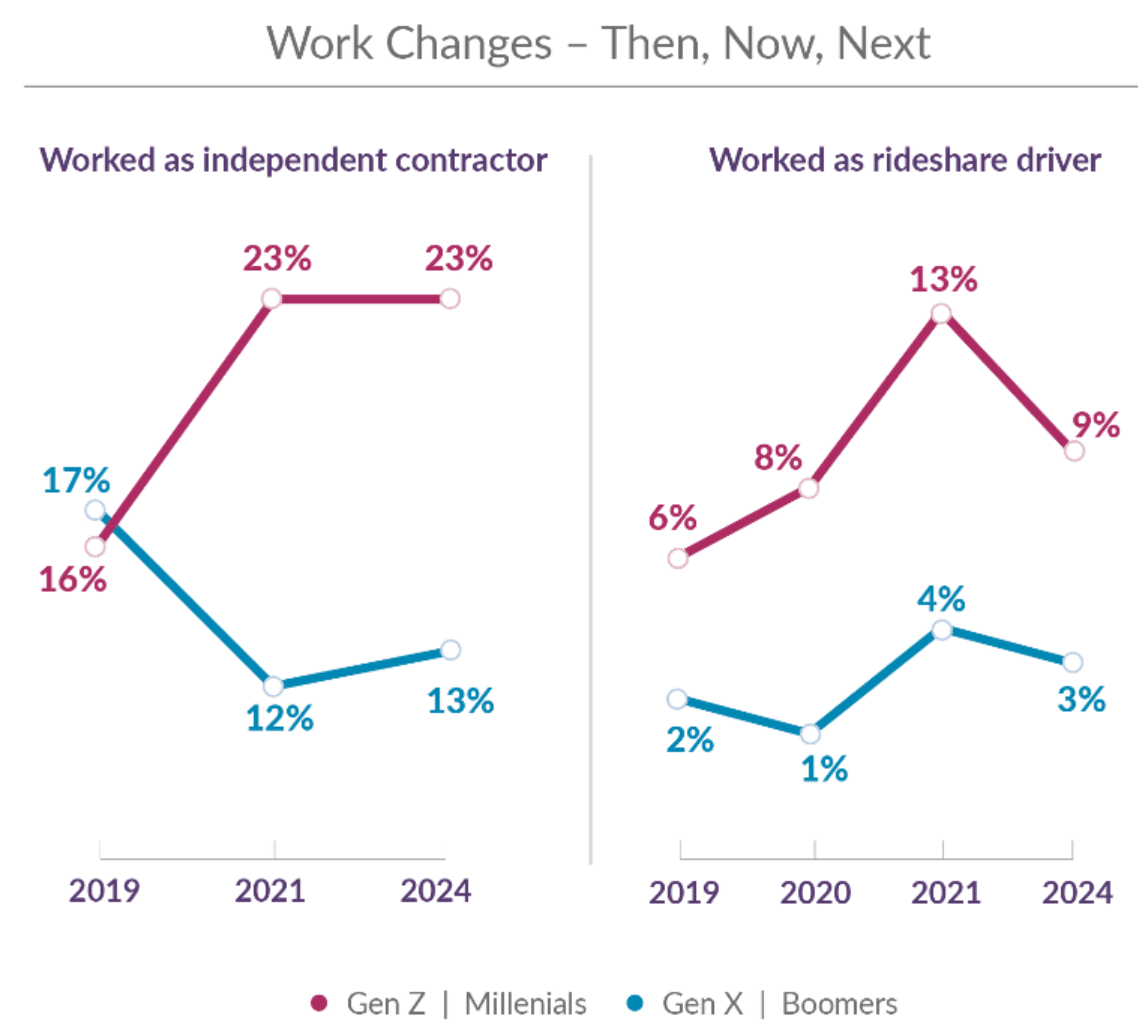

During 2020, 42% of Americans worked from home, nearly double the rate from 2019. Gen Z and Millennials reflected higher rates of gig work as both independent contractors and rideshare drivers in 2021, likely reflecting job losses, resignations from jobs and seeking new job options. (See Figure 4.) This means that geographic distribution of “the workplace” is now wider than ever before. This segment anticipates a steady continuation of independent contractor work but a decrease in rideshare work back to pre- and early-COVID levels as their employment and personal financial situations stabilize.

Figure 4: Gig economy work trends

True to this generation, Gen Z & Millennials expect to be in different jobs (45%) and working remotely (40%), continuing the transient aspects of this generation that will put new demands on employee benefits to be flexible and portable. Nearly 25% indicate they will start a business, highlighting an opportunity for insurers to develop relationships with employees directly to keep them as customers as their lifestyle changes.

These changes reflect growing opportunities for insurers to cover the shifting worker and employer needs. From on-demand benefits for gig/independent contractor work to work-from-home setups – employee and employer needs are dramatically changing. Innovative options like Nationwide’s work-from-home insurance, which bundles home/renters, usage-based auto and identify theft insurance, is an example at the forefront of this change.

Figure 5: Expected changes in work in the next three years

Opportunities in the Financial Sphere

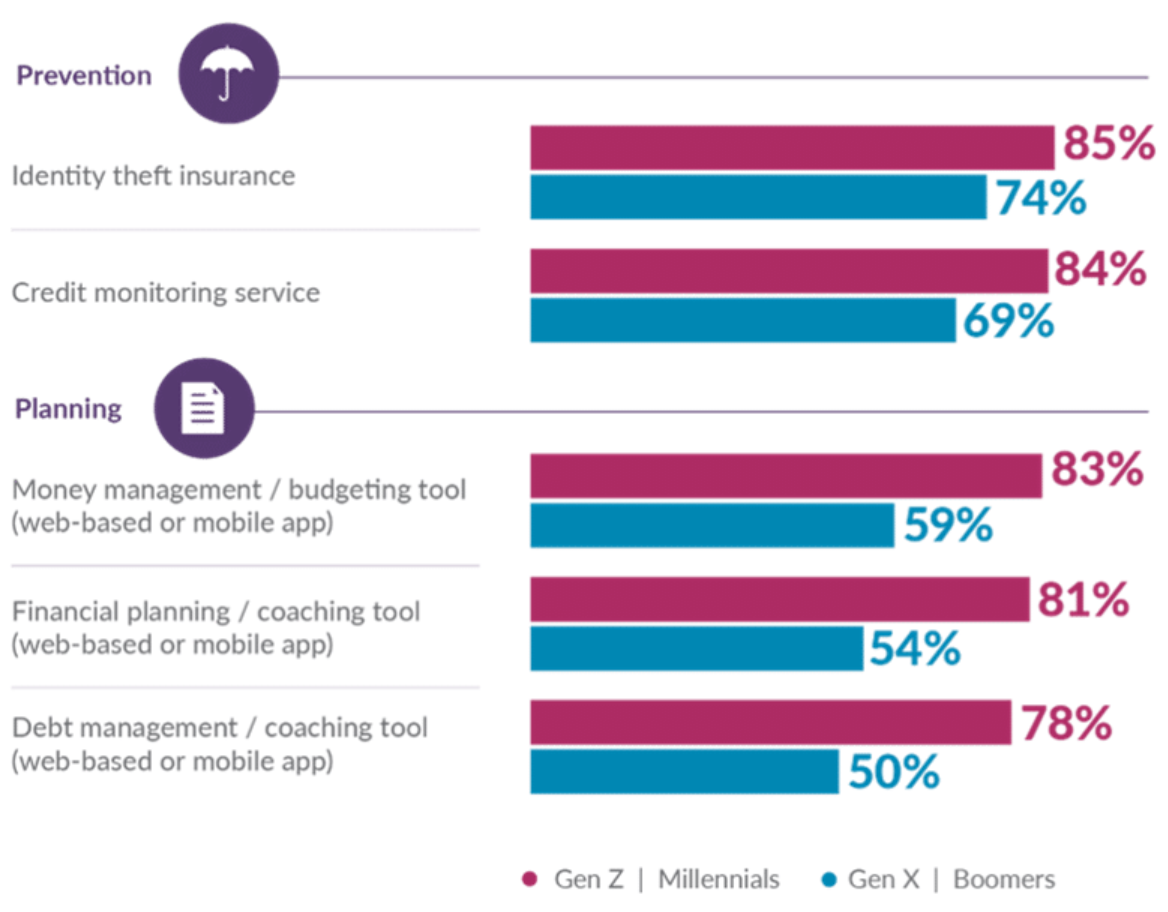

Gen Z and Millennials have consistently trailed the older generation in banking and investing by an average of 10% to 15%. This offers an excellent opportunity to engage them now to address a broader financial well-being approach by developing a partner ecosystem that brings together other financial offerings and value-added services. Insurers can take advantage of Gen Z and Millennials’ high levels of interest for both planning (money management, financial planning, debt management) and financial loss prevention and recovery services (identity theft insurance, credit monitoring) as first areas of focus for partnerships (Figure 6).

While Gen X and Boomers don’t feel the same need for planning tools or services, they are still interested in financial loss prevention and recovery services to protect their financial assets as they enter or are in retirement.

Figure 6: Interest in financial wellness value-added services

Product Placement: An Opportunity for Ecosystem and Partnership Development

For every opportunity, however, insurers will need to ascertain the best route into the market. Majesco’s research into digital shopping trends highlights the need to not just be online but to think innovatively around online positioning with partnerships in areas where people are already shopping.

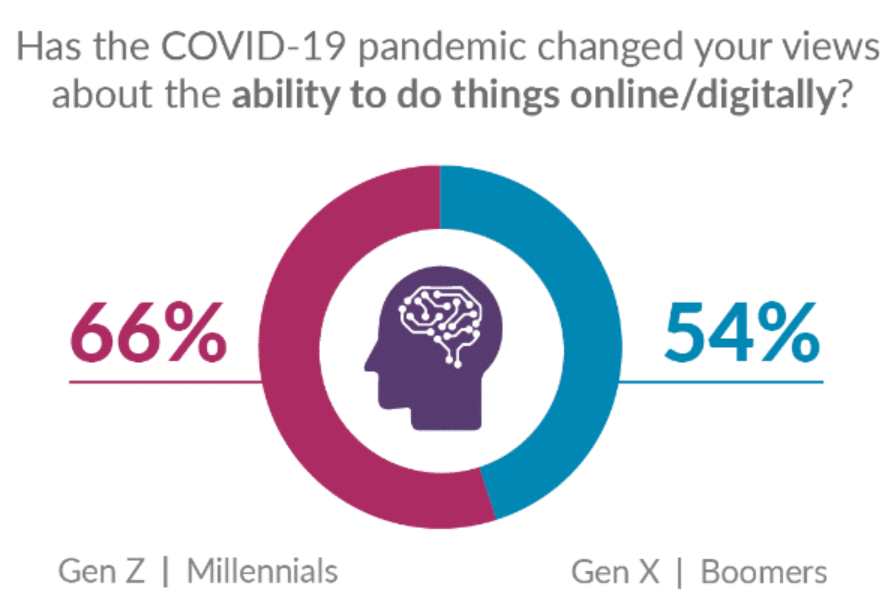

The last year has accelerated the use of digital and online options across all industries. The level of impact is substantial with 66%, of Gen Z and Millennials and 54% of Gen X and Boomers changing their views of the importance of digital and online capabilities due to COVID as seen in Figure 7. McKinsey research found that online purchases increased 30% since the beginning of COVID and have remained at this level.

Figure 7: COVID's impact on the importance of digital capabilities

And expectations continue to rise for digital and online. Both generational groups expect to do more shopping and buying online, outpacing in-store or in-person shopping by 10%. Once again, positioning is best where life happens. Carvana, for example, offers both gap insurance and mechanical protection "at the point of sale" for any car in its inventory. Are insurers prepared with the technologies and digital connectivity that will help them fill the growing gaps in online placement?

Mining the market

Just as Bitcoin was an industry to be “mined,” consumer and business trends are also filled with value for those who read the research. The viability of the insurance industry is connected to demographic trends, market trends, customer expectations and adoption of new technologies. If we lose touch with our customers, both current and future, we lose business.

Don’t miss out! You can access Majesco’s latest mine of valuable consumer information by downloading our 2021 Consumer Survey Report. And be sure to watch our recent webinar, Your Insurance Customers: A Crystal Ball of Big Changes in a Small Window of Time.